Over longer periods of time (five years or more), investments such as stocks, shares and funds have the potential to give you higher returns compared to cash savings. But the value of investments can fall as well as rise. There is a chance you may get back less than you put in. Past performance is not an indicator of future performance and should not be relied on as such. You should continue to hold cash for your short-term needs.

Overlay

Royal Bank Invest

Investment Outlook 2026: Stability in shifting landscapes

Economic impact

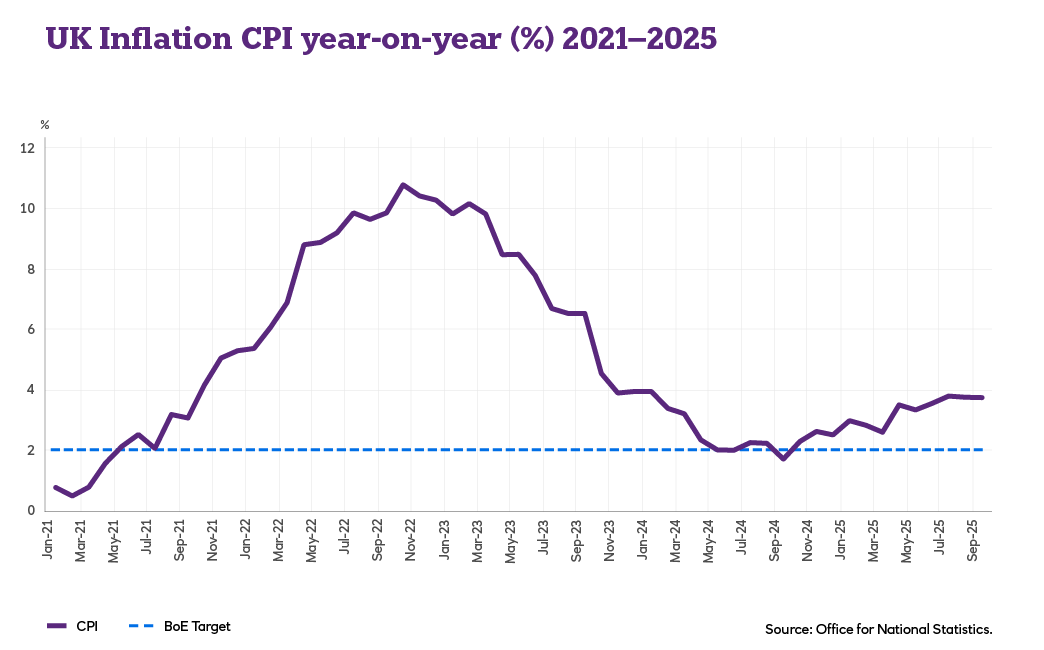

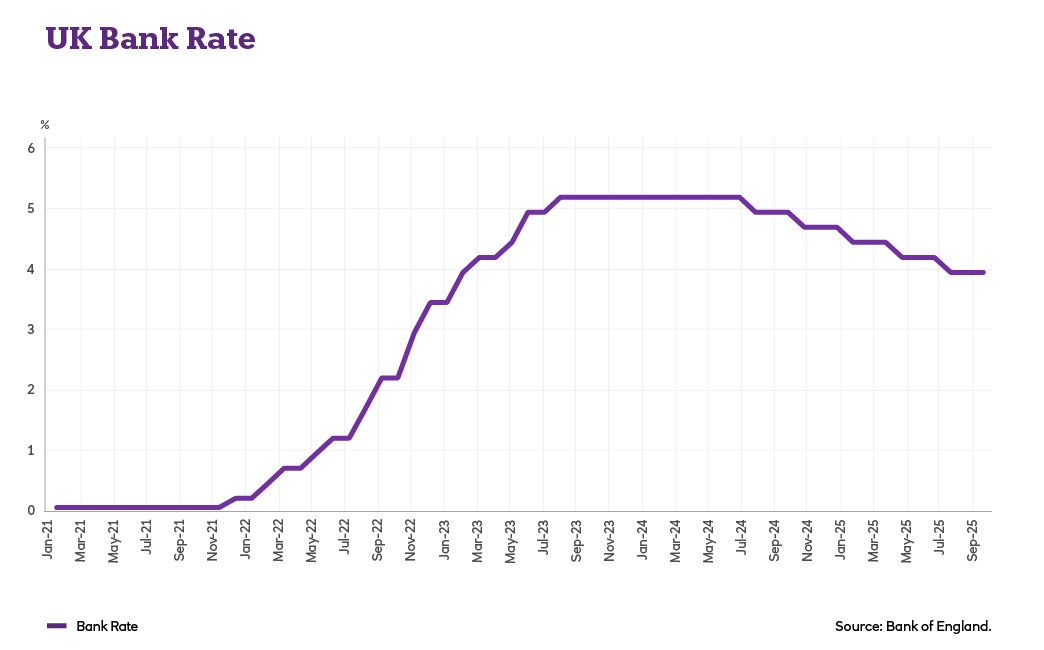

This reacceleration has prevented the Bank of England from rapidly lowering interest rates in 2025. And as higher rates generally encourage people to save rather than spend, it has also cast a long shadow over economic growth.

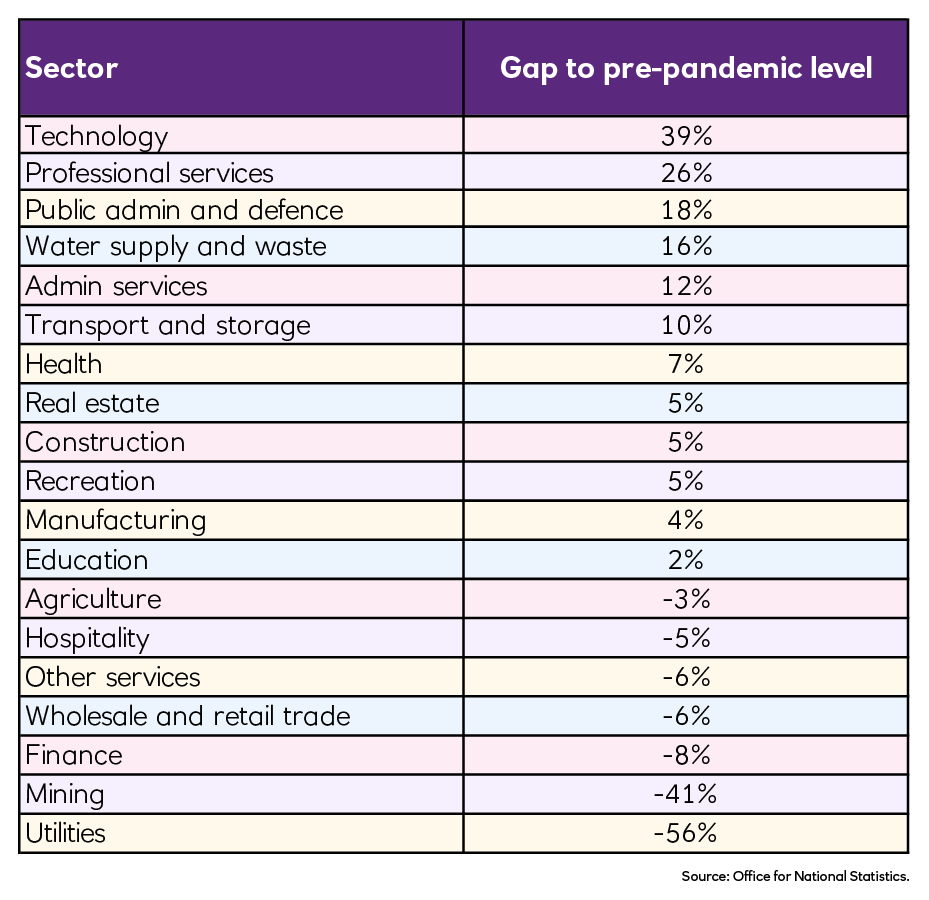

The performance of different sectors since the Covid pandemic, in terms of their contribution to economic growth, has been diverse. At the top of the table, we have technology and professional services, which grew significantly over the past five years. But sectors such as retail and hospitality are contributing 5% less than they were at the start of 2020.

Here's how much each sector’s contribution to the UK economy has grown or shrunk since just before the pandemic (for example, technology now contributes 39% more to the economy than it did in early 2020).

Household spending and savings

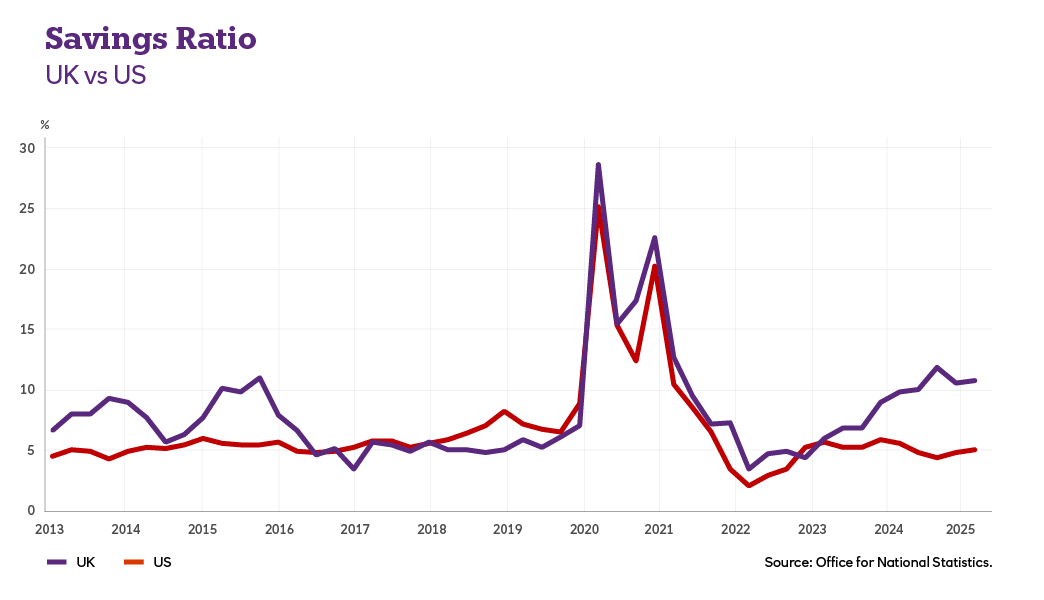

Why are people spending less on staying away, eating out and shopping?

It’s not necessarily because they don’t have the money. It may be tempting to think that in times of rapidly rising inflation we would see people cutting back on non-essential spending. But not so fast.

While prices are on average 28% higher than five years ago, wage growth has also been strong – so strong that average wages are one third higher over the same period.

It appears, instead, that Brits aren’t spending as much on those things because they prefer saving their money. UK households tend to put away more than 10% of their incomes – more than double what their US counterparts save.

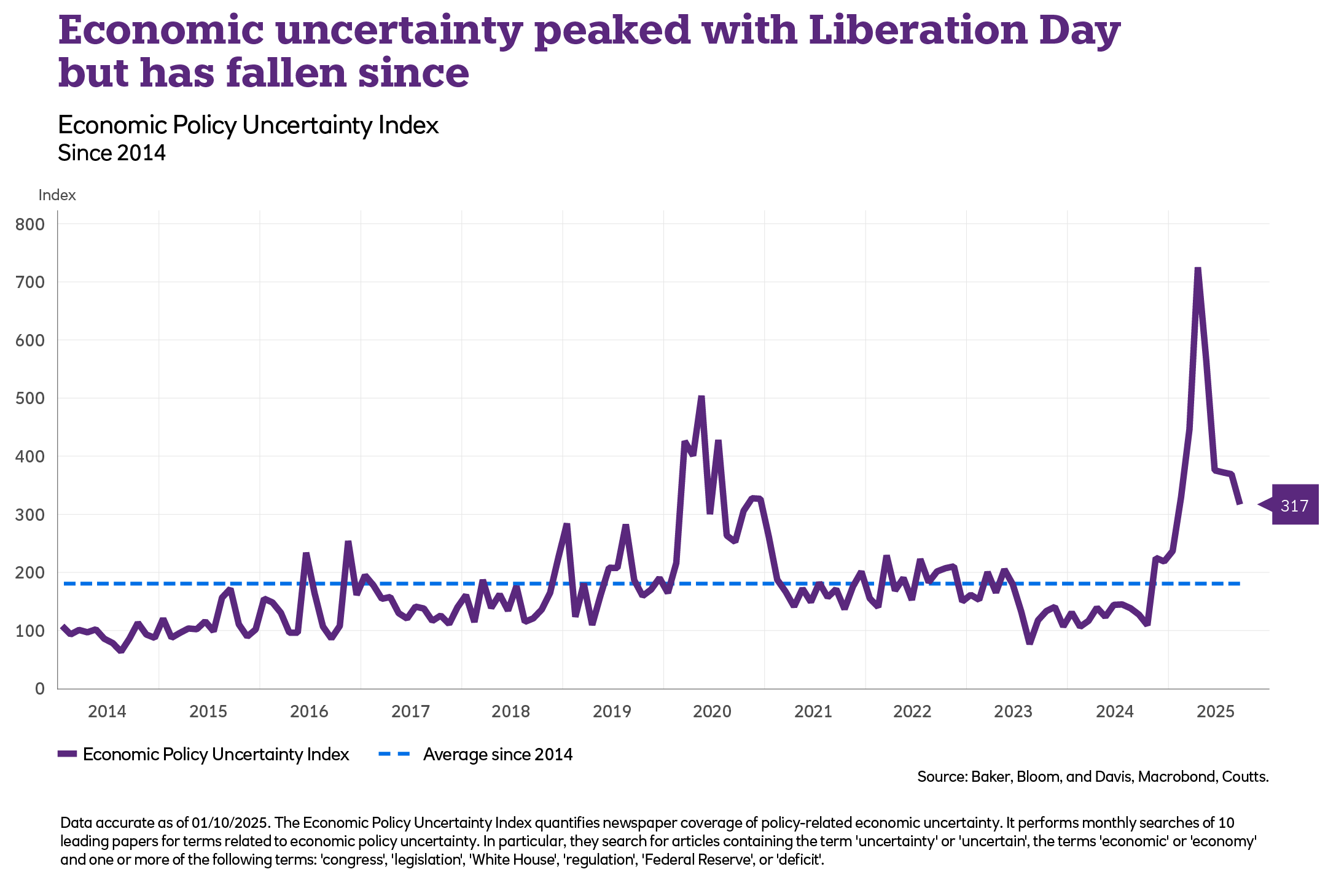

Tariffs, tariffs, tariffs

A major event was ‘Liberation Day’ in April when US President Donald Trump unveiled sweeping tariffs against all the country’s key trading partners.

While this caused a steep drop in stock markets, they quickly recovered when new trade deals were agreed. They then kept doing well despite ongoing tariff uncertainty, spurred on by resilient, positive company performance.

The rise of AI

Another big story was the growing adoption of AI. The relevant companies saw huge growth as investors embraced the technology’s potential.

Spending on AI infrastructure has helped boost the US economy, almost matching consumer spending in its contribution to growth in the first half of the year.

There were some market jitters through the second half of 2025 as concerns grew that markets might be overplaying the AI story. But investors broadly still believed in its long-term potential.

Continued economic growth

Global growth is slowing but remains positive. The global economy is expected to grow 2.9% in 2026, according to the OECD. While this isn’t a record-breaking number, it is reassuringly steady.

Information Message

Supportive government policies

Governments remain proactive in supporting their respective economies. For example, in the US, new tax cuts and the roll out of President Trump’s ‘Big Beautiful Bill’ are expected to boost spending. Elsewhere, Germany is also upping its spending on things like infrastructure after years of restrictive budgets.

Information Message

AI’s ongoing impact

AI is almost certain to remain a key theme next year. It’s still in its early stages, with just under 10% of American companies using it to deliver their core goods or services (according to the US Census Bureau). This leaves a lot of potential for future growth.

Information Message

Investment themes for the year ahead

For Coutts, the most likely scenario for 2026 is continued economic strength and solid company earnings. Interest rates are expected to keep coming down next year as well, which is typically a positive environment for stock markets.

But Coutts have also analysed what could drive even better performance next year, and where the risks are.

A more optimistic outlook could include AI creating big improvements in how companies operate, driving even stronger growth. There is the possibility of bumps along the way, like we’ve seen in the latter stages of 2025, but over time AI is expected to be a major driver of productivity.

Alternatively, risks to watch include fears around a stock market bubble – with high valuations right now – and the majority of returns coming from just a handful of technology giants.

On balance, the Coutts team believe these risks, while important, are worth enduring given how well companies are performing.

The US remains exceptional

There may be concerns about the US government's big debt and disruptive trade policies, but America remains a world leader when it comes to economic growth and innovation.

The region’s population, productivity and established institutions make it a standout among global economies. And given the strong performance of US companies throughout 2025, this momentum could carry forward into 2026.

Stocks may be getting expensive as they've done so well, but Coutts still believes there are positive times ahead and are positioned accordingly.

Information Message

Sterling is cheap versus the US dollar

Coutts believes the British pound (sterling) is currently cheap compared to the US dollar. Earlier this year they adjusted their investments to take advantage of this, increasing exposure to assets held in sterling. This means that, if US stock prices fall and the dollar is weak, it should help reduce losses because returns become worth more when converted into the UK currency.

This approach helped soften the impact of the market drops that followed Liberation Day, and supported performance when markets started recovering.

Information Message

Staying alert

As always, the Coutts team closely monitor the landscape and are ready to respond to market developments – good and bad. Their investment strategy is designed to absorb and adapt to bumps in the road while making the most of opportunities. So if anything does change, they’re ready to respond swiftly.

Opens in a new window