Free banking on everyday transactions for 2 years

Award winning start-up account ready for you

Free accounting help from FreeAgent software

Other fees may apply. Eligibility criteria, terms and conditions apply. Winner of the 2024 Business Start-up Bank of the year award at the Business Moneyfacts® Awards 2024. FreeAgent is free for as long as you retain your bank account. Optional add-ons may be chargeable.

We've got bank accounts designed for start-ups, more established enterprises and big businesses. See which one might be right for you.

Specific account eligibility criteria apply. Over 18s.

Have you got a great idea for a new business? We're here to help with all the stuff you need to get started, like business planning, and other practical bits.

We offer a range of programmes and helpful tools for businesses, plus a network of specialists who could offer help and guidance as you grow.

Whether you’re still in the idea phase or looking to grow, Business Builder is packed with practical resources. Plus, we have events to help you take the next steps with confidence.

Learn to recognise scams and protect your earnings.

Our partners could help you reduce costs and be more sustainable.

Terms, conditions and eligibility criteria apply.

Get current market trends and effective toolkits to stay prepared.

Be the first to know! Sign up to video podcasts and newsletters as they’re published.

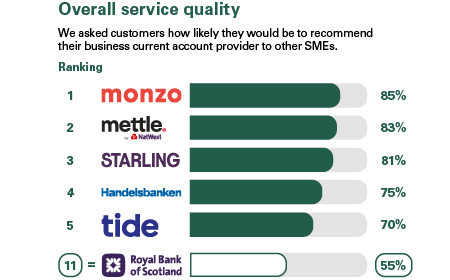

Results: 1st Monzo, 2nd mettle, 3rd Starling Bank, 4th Handelsbanken 5th Tide, 11th Royal Bank of Scotland

Results: 1st Monzo, 2nd mettle, 3rd Starling Bank, 4th Handelsbanken 5th Tide, 11th Royal Bank of Scotland

Business current accounts

An independent survey asked 1,200 customers of the 17 largest business current account providers if they’d recommend theirs to other businesses. Here are the results from February 2026.