Finances

Interest rates: how a small change can have a big impact

Managing the ups and downs of interest rates and what they could mean for your business.

29 Oct 2024

. 3 min read

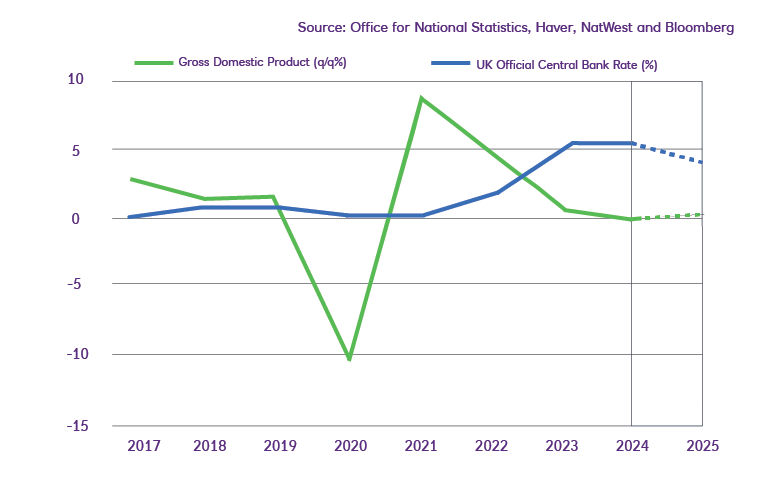

We look at how interest rates work, the difference between fixed and variable rates, and the outlook for the next year.