The UK economy was flat in Q4, avoiding a technical recession. But that doesn’t mean the worst is behind us. The economy contracted by 0.5% in December due to the effects of industrial action, while consumer-facing services suffered as people cut back on discretionary spending. The UK is the only G7 economy yet to return to pre-pandemic levels.

There were some areas of resilience: industrial output rose in December and business investment was up 5% in Q4.

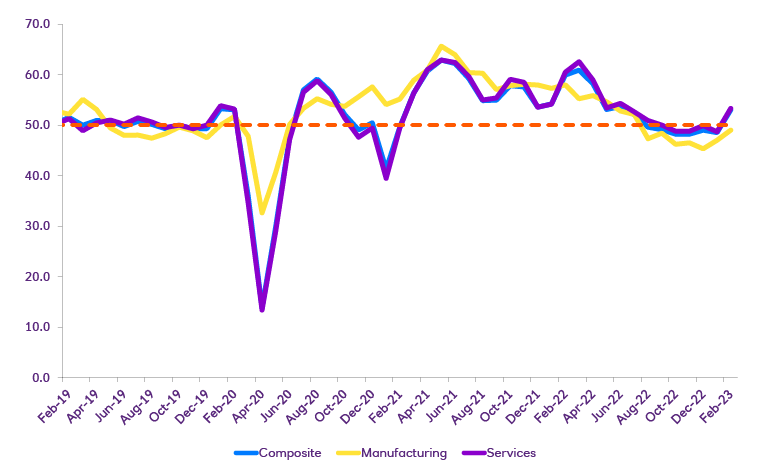

Fast-moving indicators suggest growth has regained some momentum at the start of 2023, with the UK composite Purchasing Managers’ Index (PMI) jumping from 48.5 in January to 53.0 in February. The services sector registered the biggest improvement and there are even chinks of light on the consumer side, with a more upbeat hotels, restaurants, and catering sector. And things are looking less gloomy for manufacturers, with input price pressures abating and supply chains continuing to improve.

Meanwhile, business confidence for the year ahead rose for the fourth straight month, thanks to easing cost pressures and signs of a recovery in business investment.

While all this is encouraging, the PMIs do not cover retail, construction or public services, all of which are under pressure from squeezed consumer incomes, high borrowing costs and industrial action. Household spending remains weak, and household finances continue to come under pressure. Energy grants are coming to an end and bills are still more expensive than two years ago. Higher mortgage interest payments this year will probably deduct another percentage point from annual growth in real disposable incomes. A silver lining may be that despite the cost-of-living squeeze, households have not yet drawn upon their excess savings.

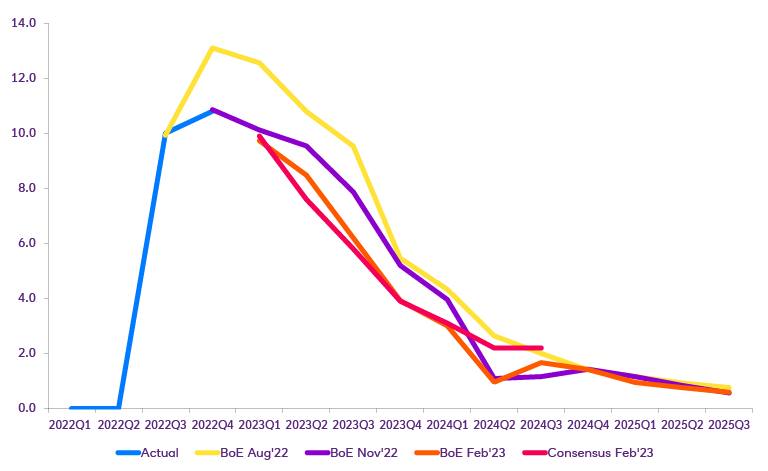

Overall, lower household spending, high borrowing and mortgage costs and likely job cuts mean economic conditions are set to remain weak. Consensus forecasts in February were for a 0.7% contraction of the UK economy in 2023.