Sector trends

Agriculture news: a 2022 outlook for beef and lamb

The Agriculture and Horticulture Development Board (AHDB) looks at the trends affecting key livestock prices into 2022.

14 Dec 2021

. 4 min read

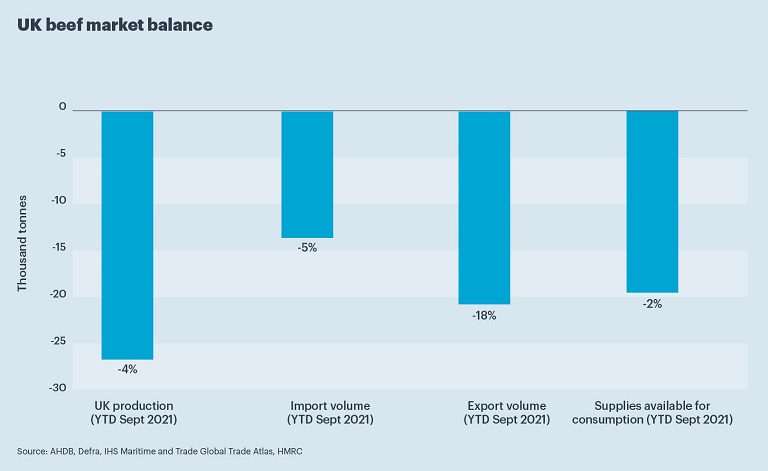

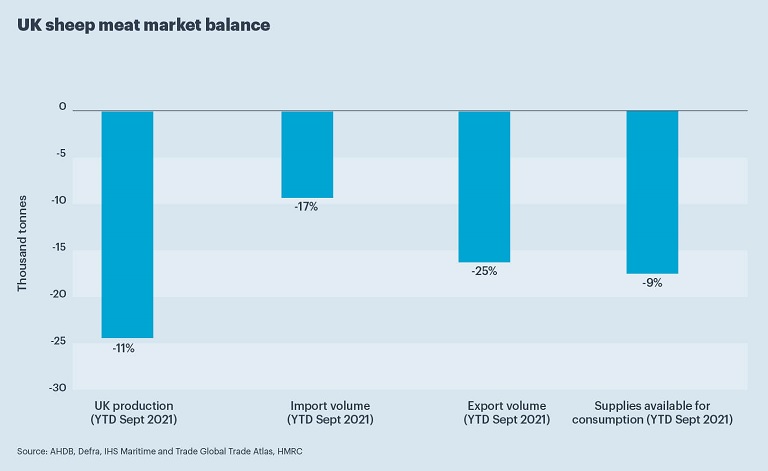

The past 18 months have been a time of uncertainty for lamb and beef producers. Worries around Brexit, the general concern over the environmental cost of red meat production and the impact of the pandemic may have loomed large, but farmgate prices of beef and lamb have remained buoyant.