Our products

Choose from our accounts with no monthly fee or view our full range of accounts.

To apply, you must be 18+ and a UK resident. Specific account eligibility criteria and fees may apply.

Like Team GB, we want to inspire and support success. Whatever your goals, together we want to get you going and keep you moving. Find out more about what the Royal Bank Team GB partnership means.

Inflation, energy prices, tax rises and the Russian invasion of Ukraine have all played a part in the rising cost of living in recent years . It's squeezing all our pockets. But we've got some handy tools to help.

There are lots of ways you can make your home more energy efficient. Doing so can save you money in the long term and could help improve the value of your home too. Check out our tips and support.

This data shows the proportion of total APP fraud losses that were reimbursed, out of 14 firms. Higher figure is better.

This data shows the amount of APP fraud sent per million pounds of transactions, out of 14 firms. Lower figure is better.

This data shows the amount of APP fraud received per million pounds of transactions, out of 20 firms. Lower figure is better.

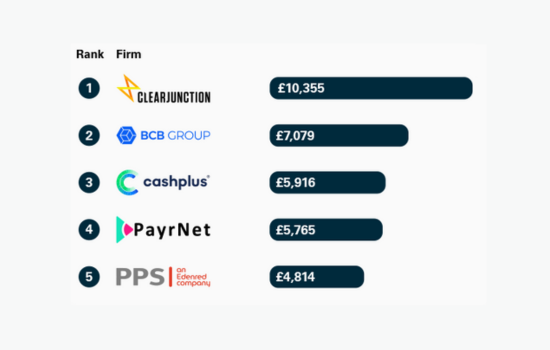

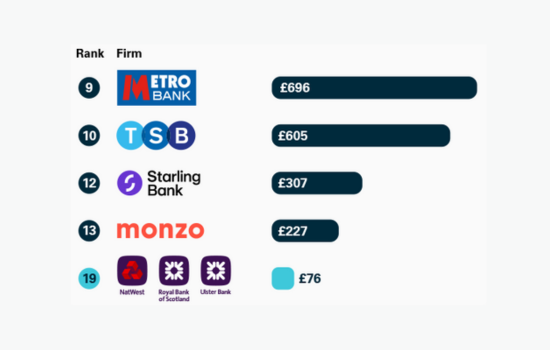

This data shows the amount of APP fraud sent per million pounds of transactions, out of 20 firms. Lower figure is better.

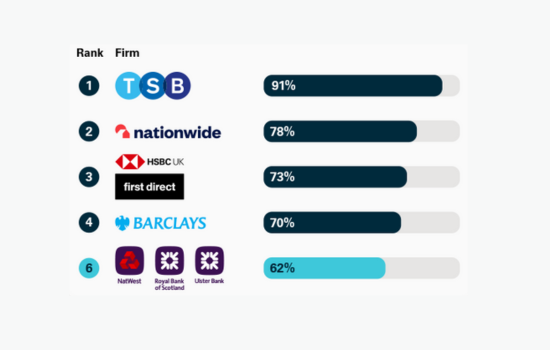

As part of a regulatory requirement, an independent survey was conducted to ask customers of the largest 16 personal current account providers if they would recommend their provider to friends or family. (Published in February 2024)

Published in February 2024